Budgeting: Crunching the Number

Learn effective budgeting strategies to achieve financial wellness. Discover tips on creating a budget, tracking expenses, saving money, and making informed financial decisions to reach your financial goals.

April 1st is many things. It’s April Fools Day, it’s my daughter’s birthday, and importantly for this article/blog, it’s the first day of the financial New Year.

Being the first day of the financial calendar, it’s also a great day to kickstart some financial housekeeping. The news about house prices going down, interest rates going up, and inflation making almost everything more expensive is, I’m sure, news that won’t have escaped your attention.

If you’re finding that your money isn’t going as far as it used to, or you are expecting your mortgage costs to double or triple, you’re not alone – and you might be feeling a little bit stressed by it.

Financial stress is very real. In fact, back in 2013 researchers from Harvard, and a host of other universities, concluded that on average, someone weighed down by money woes showed a drop in cognitive function that was comparable to a 13-point dip in IQ*. This is a similar level of impairment to missing a whole night’s sleep. (Source: here)

If you’re under financial stress it is likely to flow into other aspects of your life like work, family and relationships. The good news is that help is at hand – the banks, financial advisers, and a whole host of organisations and websites may be able to help; and one of the best ways to help yourself is to use a budget.

What is a budget?

A budget is a way to balance income, expenses and financial goals for a specific length of time.

Why is a budget important?

A good budget helps you to have control of your money – and your life too. When you think carefully about where you spend your money it creates the opportunity to improve your financial situation. For example, a good budget might:

1. Help you to pay off debt faster.

2. Help you to keep on top of your bills.

3. Help you to be more prepared for unexpected expenses.

4. Help you to save for the things that you want.

What does a good budget look like?

It varies. Some people use spreadsheets, some people use apps, some use pen and paper. They can be as simple or as complicated as you want, but something that is simple and easy to stick with is best.

(If you’ve tried to make a budget before and it hasn’t worked, I would wager that it didn’t work for one of two reasons:

1. It was too restrictive, such as going ‘cold turkey’ and cutting out all the things you love;

2. It was too complicated, meaning that it took too much time or was too hard to keep on top of)

What do you recommend?

Most of us just need a simple system to help us be more conscious about our spending - something easy to put in place and easy to stick with.

One of the best and simplest budgeting tricks I talk to clients about is a system called “Grandma’s Jam Jars”.

Grandma’s Jam Jars

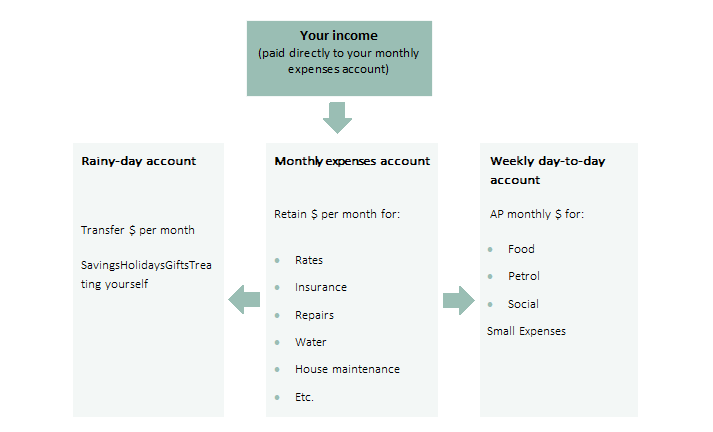

The premise is very simple. ‘Grandma’ has some glass jars for each of her expenses. On these jars, she labels each expense and the amount she needs to allocate to that jar monthly. This simple system takes the stress out of Grandma’s finances because she can always see how much money she has in each jar.

You can tailor the number of jars to your situation, but a typical example might be three jars.

Jar One: The “save it for a rainy day” jar.

Jar Two: Weekly expenses.

Jar Three: Monthly expenses.

So, what does Grandma do? Let’s say she receives $1,000 a month from her pension, that her mortgage and household bills are $500 a month, and her food and petrol costs are $250 a month.

Firstly, she takes all her pension and puts it into her “monthly expenses” jar every time it gets paid. This will cover bills that are non-negotiable. Things like mortgage payments, rent, phone bills and power. ($500 per month).

Second, she takes out of this jar what she can afford to put into her rainy-day jar. She sets this money aside for savings, unexpected events, Christmas presents and holidays. ($200.)

Finally, she takes from the first jar what she needs to cover weekly living costs. Food, petrol, and the like ($250) and adds a little extra for entertainment and social events ($50). (So, $300 in total).

The catch is that when her weekly living jar gets low, she knows that she must limit her spending until her pension gets paid next. If she only has $20 left in the jar after three weeks of groceries and petrol, she knows that she needs to make it last.

It’s a simple system – but it works. Doing this with real jam jars and cash like grandma does makes it very easy to see how much you are spending and how much you have left. Nowadays, most people pay by card rather than cash, but the exact same thing can be done by setting separate accounts up with your bank.

A diagram below:

In my experience, almost every person who is in control of their finances has a system for day-to-day cash management. It is the rock on which all other financial strategies are built. The old saying “If you watch the pennies the pounds look after themselves” can be true.

If you already have a system, then congratulations. You probably feel in control. It you don’t then why not give this a try. There is nothing to lose and it might be the thing that makes all the difference.